Wow, this week was challenging with Wednesday being the worst. The middle the week I had to do some damage control on some of my positions. As a result, I took off some obvious winners to free up some buying power so I could take advantage of the nice sell off. This helped bring my buying power back in line as it was north of 50%.

Below is the winners I took off on Tuesday to free up some buying power.

Another position took off the $MA roll from the week prior for a gain of $178. This is all the good news. Unfortunately, the damage done on Tuesday and Wednesday forced me to make a few tough decisions. In the past these have proven to be “gotcha” moments. I’ll explain in a second.

$SPOT $NOW and $MU were getting close if not ITM. Especially $SPOT and $NOW. When looking at a chart on both of these positions, they both looked really weak. Almost as if they were going to drop off a cliff. $SPOT expired on Friday. My thinking was I could just hold out a few more days and see if it recovers. That comes at a great risk however. I call it the “drip” vs. “flood gate” phenomenon. Meaning, closer the expiry approaches, the more damage that can be done if it goes against you or ITM. That is exactly what happened in this case. The market sell-off caused $SPOT to go ITM and this thing ballooned to a huge loss quickly. Even if it was only 1 day to expiry and only ITM by a buck, it would still be down significantly until expiration Friday where it could teeter todder ATM between big loss or no loss. This is one reason why I stopped selling to open 7-14 DTE options. I now go out 30-45 days with hopes of closing them 10-14 days prior to expiry. This should solve the “drip” vs. “flood gate” issue for the most part.

Made a judgment call and I decided to take the loss on $SPOT. The loss was much greater. I felt I got away with murder here with the loss that I did. Come to find out, it closed Friday OTM. This has happened many many times over the last few months. Taking big loss on something that ended up going OTM at or prior to expiry.

What is the solution to prevent that or at least reduce this? Well, obviously stock selection, strike selection (using a chart for support/resistance), but, I’d say that going out 30-45 days should help with this. Another thing you could do is just take the loss early before it gets rather large. Even if the option has extrinsic value left in it or could go OTM prior to expiration. I think this is still a case by case basis. Had this been $MSFT or $APPL, I probably would of let it ride until expiry. But, I didn’t feel comfortable doing that with $NOW $SPOT, or $MU.

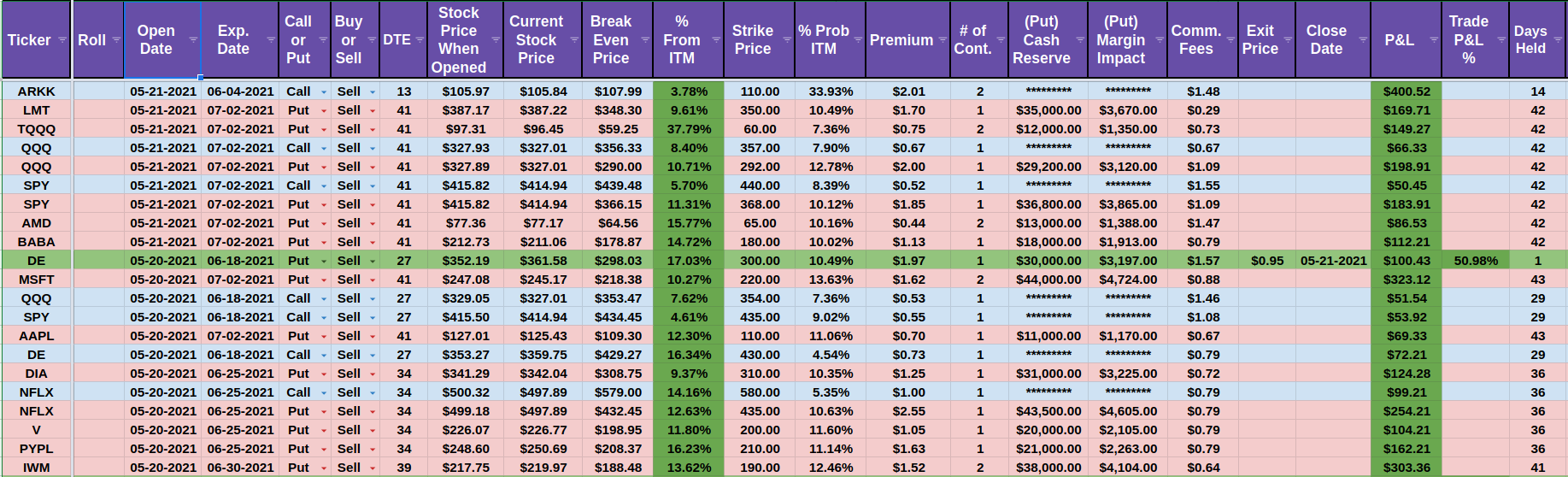

With being out of harms way and market recovering, I took advantage of the buying power available and put on the following.

As you can see, I started to build out Jun 25 and July 02 now. Eventually I’ll fill in week to week going out 30-45 days. If I take something off going forward, I’ll put on a new position going out about 45 days. Going forward I should be able to take positions off each week that had been on for 30-45 days depending.

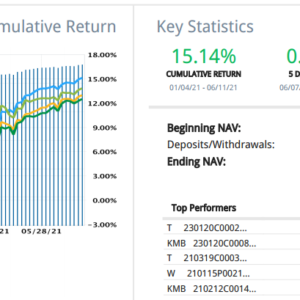

Here is the list of current positions and account health.

HF

Latest posts by HF (see all)

- Thetagang Options Week of 06-14-21 - June 20, 2021

- Thetagang Options Recap Week of 06-07-21 - June 13, 2021

- Thetagang Options Recap Week of 06-01-21 - June 6, 2021